Pakistan Reader# 221, 4 October 2021

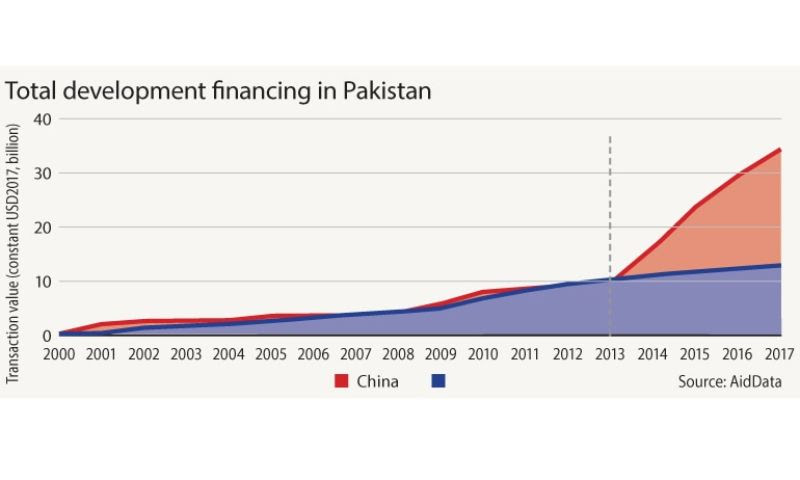

On September 29, AidData, a US-based international development research lab released a report, Banking on the Belt and Road: Insights from a new global dataset of 13,427 Chinese development projects. The report discussed banking practices conducted by China’s sovereign banks and State-Owned Enterprises. The report compared the nature of grants, loans and assistance under the two heads, Official Development Assistance (ODA) and Other Official Flows (OOF) before the launch of the Belt and Road Initiative (BRI) and after the launch of BRI. The difference between ODA and OOF is established in terms of varying lending rates (commercial lending rates under the latter) for the loans and respective repayment safeguards. In the case of Pakistan, as per the report over the period of 2000-2017, Pakistan received ODA amounting to USD 4.18 billion and for the OOF the loans amounted to USD 27.84 billion. However, Pakistan has invented its special mechanisms of repayment through return on equity rate from special purpose vehicles (SPV), for example, Gwadar Port Authority will share 91 per cent of the revenue generated through services. Private sector institutions (independent power producers) have also been roped into payment guarantees especially in power-related projects under China Pakistan Economic Corridor (CPEC).

Findings from the report

The report and analysis by AidData come out with four conclusions.

First, there is a pattern of larger preference of giving assistance through OOF rather than ODA in overall BRI projects, in OOF the ratio of loans to grants post the introduction of BRI is 31:1 while that under ODA the ratio remains 9:1. The amount of every dollar lent under OOF was 5.3 times that under ODA, after the launch of BRI, China spent 9.1 dollars of OOF for every dollar of ODA. The color of money going out from China has also changed to commercial from concessional for Asia, Africa, Central Asia and Latin America as well. Chinese financial commitment for Pakistan increased by 346 per cent over the two periods, pre and post BRI launch. The total committed amount by Pakistan under CPEC has been fluctuating, Ishrat Hussain maintains the commitment at USD 50 billion under two broad categories, USD 35 billion for energy projects and USD 15 billion under infrastructure projects. The projects under energy capacity development are completely under foreign direct investment routes and financed by the private company from China Development Bank and China Exim Bank against their own balance sheets, under independent power producer (IPP) mode. Therefore, the debt is to be borne by Chinese investors and it won’t be an obligation on part of the Government of Pakistan.

Second, loans (foreign currency-denominated) under BRI projects have been collateralized against future commodity export receipts to recover the amount, this will hugely supplement the currently stagnant export market of China but this will hurt the low to middle-income country’s (LMIC), whose export profile is still in nascent stages of manufacturing or finished goods rather than services. In the case of Pakistan, there has been no public announcements of such a repayment mechanism but if such a method exists, it might be very risky to the competitiveness of its primary and secondary industries against cheap steel, agriculture and consumer goods.

Third, there has been gradual stronger loan repayment safeguards due to increased credit risks associated with long term and short-term profitability of the projects. For example, the Hambantota port has been leased to a private company of China due to the failure of the Sri Lankan government in repaying debts.

Fourth, the report points out the increasing hidden debts, which do not get accounted for in the balance sheet of the countries. The debt reporting system (DRS) of the World Bank hence is not able to account for the correct credit risks existing in the countries engaged in BRI projects, especially LMIC. As per the report, loans worth USD 385 billion lie in the hidden debt category. In the case of Pakistan, the hidden debt as of 2017, stands at 8% of the GDP whereas the sovereign debt stands at one per cent only.

The report rightly makes a fundamental distinction between western investments and Chinese investments, the former being software investment while the latter being hardware investments (infrastructure, port development, energy projects) as upon the completion of the project(s), the project will have to turn profitable which can come out only from the conducive economic environment in terms of enhanced economic activities and employment generation in the host countries. In the case of Pakistan, the Gwadar port and western section of CPEC passing through Balochistan have not generated enough opportunities for the people; there have been protests by fishermen in Gwadar over the government allowing Chinese trawlers to fish. The fishing techniques have not been upgraded to the scale of Gwadar development while fishermen had given up their land for the development of the port. Some up-gradation of traditional knowledge with the latest techniques in fishing would have subdued such dissent from the inhabiting population of Gwadar.

There is an interesting table in the report, whereby Pakistan tops the list of countries where BRI projects are facing some nature of the problem, be it scandals, controversies, or alleged violations. The ten problematic projects amount to USD 5.675 billion in Pakistan followed by Indonesia with 9 problematic projects under BRI. ‘Special Security Division for Pak-China Economic Projects’ has been set up, it has brought extraordinary expenses for the country already suffering from a fiscal deficit and circular debt problem of the power sector. There is some ecological respite as well, energy projects through renewable energy have also been floated with return on equity mechanism and payment guarantees through independent power producers endorsed by Central Power Purchasing Authority Pakistan.

References

Malik, A., Parks, B., Russell, B., Lin, J., Walsh, K., Solomon, K., Zhang, S., Elston, T., and S. Goodman, "Banking on the Belt and Road: Insights from a new global dataset of 13,427 Chinese development projects," Williamsburg, VA: AidData at William & Mary, 2021

Kazim Alam, "Most loans under CPEC at commercial rates: report," Dawn, 30 September 2021.

Khurram Husain, "Hidden costs of CPEC," Dawn, 29 September 2021.

Ishrat Husain, "Financing burden of CPEC," Dawn, 11 February 2017

Amir Wasim, "Govt bulldozes CPEC Authority bill through NA," Dawn, 2 February 2021

D Suba Chandran, "Protests in Gwadar: Who and Why," Pakistan Reader, 1 October 2021

Khaleeq Kiani, "5 CPEC power projects face delays," Dawn, 3 August 2021.

Iftikhar A. Khan, "China to get 91pc Gwadar income, minister tells Senate," Dawn, 25 November 2017

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)