Pakistan Reader# 709, 8 January 2024

On 8 January, an editorial in Dawn titled Sombre outlook analyzed Pakistan’s economic prospects based on the recently released United Nations’ World Economic Situation and Prospects report for 2024. The editorial states that this report has “painted a sobering picture of Pakistan’s economy as it continues to face multiple challenges, including inflationary pressures, currency depreciation, and high levels of sovereign debt.”

The world economic situation

The UN’s flagship report mainly delineates international economic trends and has identified some key “short-term risks” and “structural vulnerabilities” for the world economy. These are:

It is no wonder then that the report has projected “the global GDP growth to slow from an estimated 2.7 per cent in 2023 to 2.4 per cent in 2024.” The report further states that growth is likely to “improve moderately to 2.7 per cent in 2025 but will remain below the pre-pandemic trend growth rate of 3 per cent.” It has argued that the world will witness a “protracted period of low growth.” It is in this international economic context that the report’s projection for Pakistan and the latter’s challenges must be analyzed.

Key takeaways for Pakistan

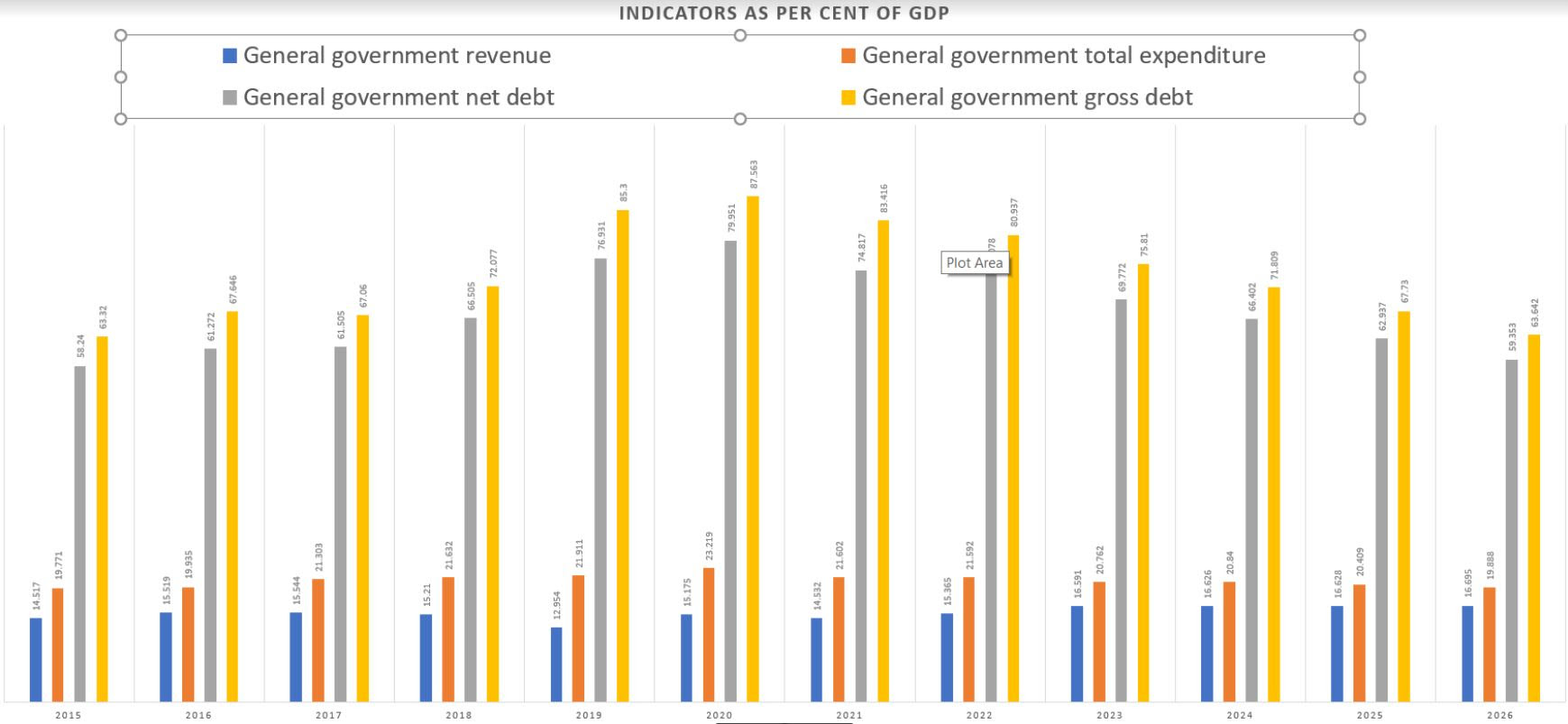

1. Inflationary pressures: Pakistan has been reeling under the effect of rising inflation with the rate skyrocketing to 39.18 per cent in 2023. This has prompted the State Bank of Pakistan to increase and maintain a high policy rate of 22 per cent since June 2023.

2. Currency depreciation: Pakistan’s currency depreciated by over 20 per cent in 2023.

3. High levels of sovereign debt: Pakistan has amassed a substantial amount of sovereign debt that threatens its debt sustainability. External debt for the year 2023 amounted to 36.5 per cent of the country’s nominal GDP.

4. The report has warned of a potential rise in food insecurity.

5. Pakistan is also dealing with its most serious balance of payments crisis

With the country grappling with these myriad challenges, it is not surprising that the report has pegged Pakistan’s growth rate at around two per cent this year and a slightly improved 2.4 per cent in 2025. This projection is similar to that made by other institutions like the International Monetary Fund and the World Bank. This modest growth rate, however, is “a slight improvement over an economic contraction of 0.2 per cent during the last fiscal year ending on June 30, 2023.”

What can be done?

With the report painting a glum picture of the international economic situation and within Pakistan, the editorial has argued that “the current crisis also offers a major opportunity to the country’s policymakers to reset the economic policy direction and fix the long-standing structural issues dragging down the country.” The editorial further argues that Pakistan must learn from countries like India, Malaysia, the Philippines and Turkey who in times of deep economic crises in the past “put their economies back on sustainable, long-term growth trajectories.” It can be argued here that any course-correction requires bold and relevant long-term policies which depend on the presence and willingness of strong leadership. Another key prerequisite for a policy shift is political stability followed by good governance. With the general elections round the corner, Pakistan is at cusp of a unique opportunity to break from its tumultuous past into a future that it can sculpt with acumen and with the interests of its people in mind.

References

Anwar Iqbal, “Pakistan’s economy to reel under global challenges in 2024, says UN report,” Dawn, 6 January 2024

“Sombre outlook,” Dawn, 8 January 2024

“World Economic Situations and Prospects 2024”

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)