Pakistan Reader# 457, 9 December 2022

On 8 December, the State Bank of Pakistan’s (SBP) foreign exchange reserves dipped to USD 784 million to a fatal four-year low of USD 6.2 billion in the week that ended on 2 December. The SBP’s reserves on 18 January 2019 were a total of USD 6.64 billion which caused a major drawback to the country’s economic policy agenda. The SBP’s reserves have dropped by more than USD 4 billion from USD 10.9 billion in April of 2022, and have resorted to inadequate policies and replenishment since its dip. Experts cite that the falling reserves will “make it more difficult” for Pakistan to repay its foreign loans while saying that the remaining purse of USD 6.7 billion is “just enough” to cover a month’s imports.

On the same day, the SBP’s Governor Jameel Ahmad reassured the international community that the country would make its maturing debt repayments on time and that the bank only owes USD 4.7 billion over the next seven months. Ahmad stated that loan repayments have been in line with the country’s foreign exchange reserves and that they are “more than sufficient” for the next fiscal year of 2023. He noted that two commercial banks are meant to re-lend USD 1.2 billion in the next few days and that Pakistan’s foreign exchange reserves will come up to nearly USD 8 billion, which has been a 4-year low from USD 6.7 billion.

What did the SBP say on dipping reserves before December 2022?

On 3 April 2022, the SBP recorded the trade of the US dollar at PKR 184.09 rupees, slashed the Pakistani Rupee of its value by 3.2 per cent only against the US dollar, and left the local currency at a stifling pressure point. Economic and trading analysts had termed the move to be “out of control” and said that the SBP had “lost confidence” in getting the exchange rate back on track after losing nearly USD 8 billion in the first eight months of the fiscal year of 2022.

With import bills rising up by 49 per cent in July-Feb in 2022, the bill amounted to nearly USD 50 billion, with the dollar not resisting volatility for the sake of stability in the exchange rate of the Pakistani Rupee. Two months after the staggering devaluation, the SBP dismissed claims that the country’s foreign exchange reserves had “dried up” and assured that the country’s reserves are “fully usable for all purposes.” At the time, Pakistan’s reserves had fallen by USD 234 million to close below USD 15 billion, with the SBP’s share amounting to little less than USD nine billion.

Why have the foreign exchange reserves dropped?

Ahmad explained that the country’s reserves had decreased to a “critical level” after the repayment of two commercial loans, which were an addition to the return of the USD 1 billion against a matured Sukuk loan on 2 December of this year. He said that the foreign currency inflows are meant to come in the second half of the 2023 fiscal year and the government is planning to acquire USD 3 billion from a “friendly” country and that the reserves would increase over time. He emphasised that there is “no concern” over immediate repayments and that they will be made “successfully.”

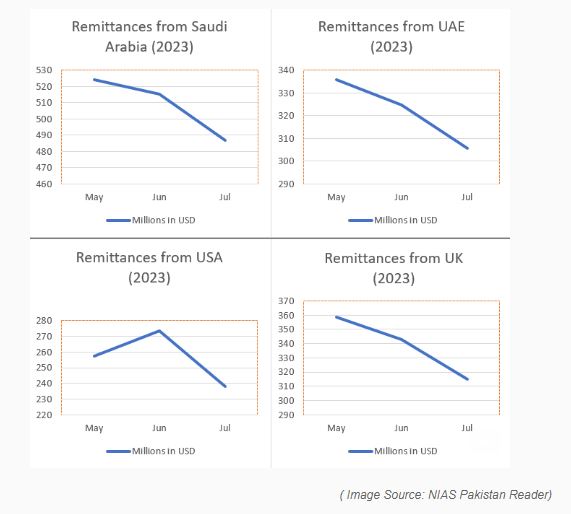

He admitted that the country is facing varied challenges in external and internal economic areas, and the increase in global commodity, fuel, and gas prices has fuelled high inflation prices across the world, including Pakistan. He said that the SBP’s plan of action for the current account deficits has remained unchanged at 2.5 per cent of the GDP in the fiscal year of 2023, “despite the devastation caused by the floods.” This comes as Pakistan’s foreign currency inflows sent to the country by overseas Pakistanis through their Roshan Digital Accounts (RDAs) have hit a 23-month low amounting to USD 141 million in November 2022, and have led to a gross inflow amount of USD 5.4 billion in the last 27 months.

The SBP’s downplaying brings to light a serious concern for the country’s reserves in the future as it refutes the high rate of return in countries that it owes money and the political instability that it is plagued by. The SBP’s loan rollover leaves a trail of mistrust in the market, with trade deals sealed off at higher prices, the demand for dollars remaining high, and the political cost of imposing higher taxes for higher revenues curtailing the bank’s cohesiveness to tackle the issue. (Shahid Iqbal, “SBP’s forex reserves fall to near four-year low,” Dawn, 9 December 2022; Salman Siddiqui, “SBP downplays risk of default,” The Express Tribune, 9 December 2022; Tahir Sherani, “SBP clarifies its foreign exchange reserves have not dried up,” Dawn, 21 June 2022; Shahid Iqbal, “Exchange rate spirals out of SBP’s control,” Dawn, 3 April 2022)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)