|

On 4 October, sixth review talks began between Pakistan and the International Monetary Fund (IMF) for disbursement of loan tranche of USD 1 billion under Extended Fund Facility (EFF) program. The talks scheduled from October 4 to 15 remained inconclusive so far at the staff level agreement due to different priorities of the two sides. This is the twenty third time when Pakistan has gone to the IMF for a bailout and to improve fiscal management. The conditionalities of IMF programs have grown harsher in macroeconomic policy targets for every new fund facility agreed between Pakistan and IMF.

Background

Upon taking over charge the new government under Imran Khan initially avoided opting for IMF fund facility to deal with forex reserve crises but ended up agreeing to an EFF worth USD 6 billion. The latest discussions are the final round of review talks to complete the last leg of tranche of the total loan amount of EFF, in return for such cheap loans, the agreement mandates Pakistan to achieve some economic targets and gradual structural reforms. Some of the targets under the latest arrangement were a rise in base electricity tariff, reducing subsidies and tax exemptions for fiscal discipline, improved tax collection targets, controlling circular debt of the power sector, restructuring or privatization of state-owned-enterprises and rationalization of petroleum prices.

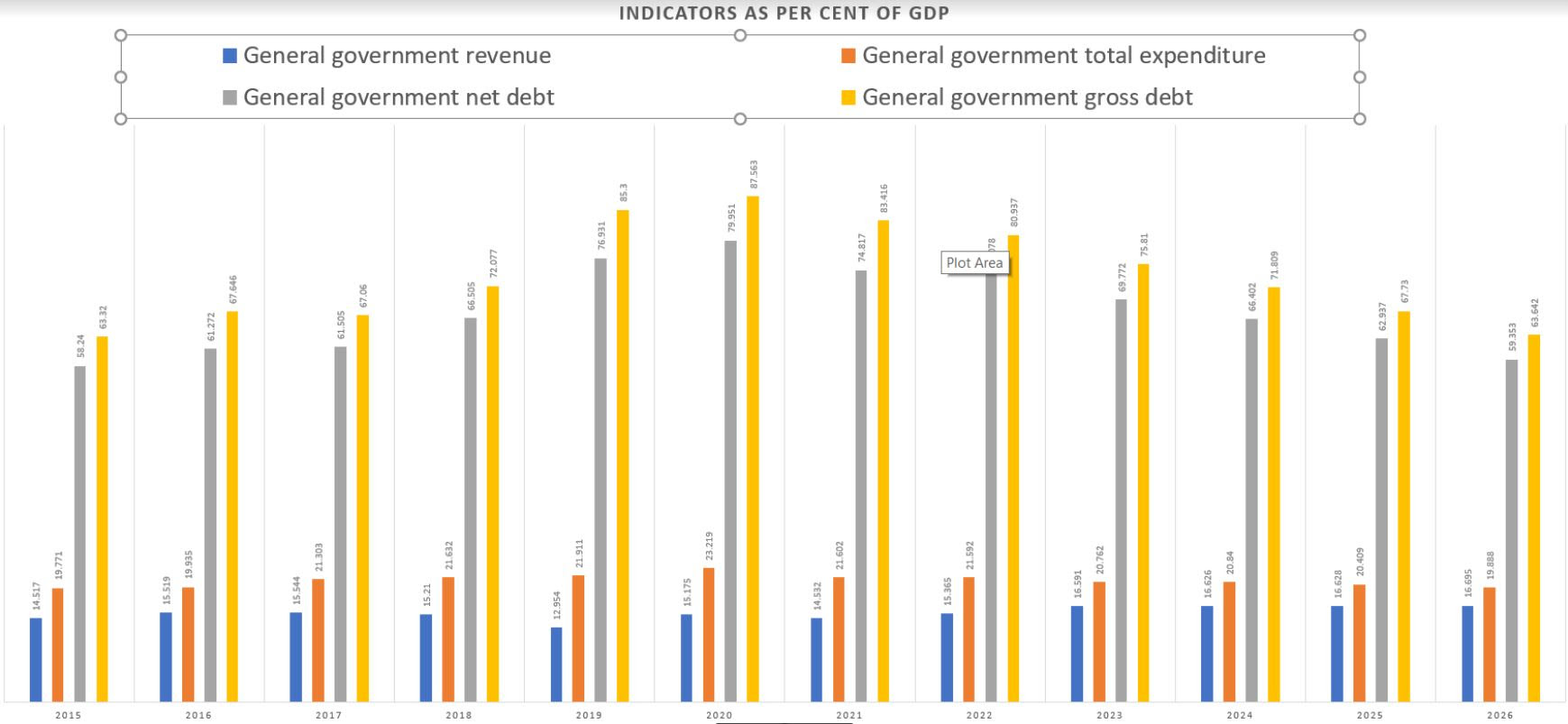

Currently, Pakistan does not have a major problem of current account deficit or even forex reserve crises, the GDP growth projection has been revised in a positive outlook to around four per cent. The country has seen robust consumption activity since pandemic began to reside, since Pakistan is a net importer of consumer commodities, the import graph has begun to rise again against stagnant exports supplemented by a record surge in remittances. The market led exchange rate floating of domestic currency is bringing price parity with international prices but this rise of PKR from around PKR 150 per dollar to PKR 175 per dollar within a span of six months has hurt the general public the most. But that is not enough for the financial masters at the IMF. The focal locations of Pakistan and IMF are certainly not matching to reach a consensus, IMF has a straightjacket approach to macroeconomic wellness and Pakistan due to its peculiar location and history of maladjusted governance has transformed the nature of lending itself. As per a document of July 2019, additional financial liquidity from friendly nations to Pakistan can help achieve the program objectives, this hints that the nature of lending from IMF is transforming from bilateral into multilateral axioms.

Why is IMF approval significant?

Before every review meeting, the borrowing country is expected to submit the progress report and subject to satisfactory approval by IMF staff, the IMF boards approves the continuance of the fund facility. By looking at the amount of loan one may wonder about the significance of the quantity of the loan, a paltry USD 6 billion? But the significance is in the quality of approval. An approval and all good indications by IMF staff reflect credibility of a country in economic growth, its resilience to sustain market shocks, and most importantly to avoid defaulting on previous cyclical loans repayments as in those conditions the borrowing becomes expensive due to perceived lack of trust. So, IMF progress reports and summaries about a country act like a standardization of economic wellness of a country. It is very unfortunate that economic wellness is only measured in terms of government revenue collecting capability, tax to GDP ratio rather the focus needs to be kept at governance indices, human development indicators along with fiscal indicators.

Currently inflation in Pakistan is around 14 per cent; this has resulted in misery and hunger crises for the most vulnerable people, the country’s human resources are left bereft in one way or the other, this time the masses are at the helm of market led exchange rate and inflation. Political parties have kept on relying on loan programs of the IMF periodically to address the structural problems ailing the economy. Recently, the IMF resident representative of Pakistan had called on the Auditor General of Pakistan and held discussions about progress and status of covid related expenditures, this incident hints at the lack of trust cemented in IMF staff members over time. Such a complex situation has kept Pakistan's economy in a fizz, boosted by IMF financial steroids periodically. It may keep the geopolitical ambitions floating but in the long run the national power may not remain as comprehensive as it is aspired to in the commitments to the IMF.

References

“Chickens always come home to roost,” Business Recorder, 25 October 2021

“Saudi Support and IMF Programme,” Business Recorder, 28 October 2021

Anwar Iqbal, “Pakistan-IMF talks remain inconclusive, so far,” Dawn, 23 October 2021

“IMF official calls on AGP,” Business Recorder, 19 October 2021

|

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)