Pakistan Reader# 496, 3 January 2023

On 3 January, the Pakistan Bureau of Statistics (PBS) released the monthly data for December 2022 and said that all the commodities that make the consolidated consumer price index (CPI) showed a climbing trend, except for perishable items. The PBS said that the “most damaging impact” was from the food sector, with inflation and price rises amounting to nearly 35.5 and 56 per cent this month. The PBS remarked that even though the CPI general inflation rate had decreased to 23.8 per cent in October, the decline remained short-lived and totaled to about 24.5 per cent in December.

The PBS outlined its report on the basis of how much inflation has affected urban and rural sectors in the economy and said that on a year-on-year (YOY) basis, the urban inflation rose to 21.6 per cent in December as compared to 17.6 per cent in the previous year. Additionally, the rural CPI escalated to nearly 28.8 per cent on a YoY basis in December as compared to 11.6 per cent in December 2021. The PBS said that the “pace” in inflation was measured “in line” with the outlook proposed by the Ministry of Finance, which forecasted average inflation between 21-23 per cent and that the urban inflation rate measured without the unstable food and energy prices stood at 14.7 per cent.

What are the implications?

First, the aftermath of an overheated and disordered economy has left the government unable to force its priorities to adapt quantitative measures to tighten the market from a further escalation into economic disdain. The market is at a particularly vulnerable state, with inflation reaching a 40-year high after the sustenance of an aggressive policy by the government. The government will have to further support the USD rather than sell them, keeping in mind that the USD will encourage investment and stability in the country.

Second, extensive damage from the floods. Nearly 40 per cent of the entire crop system of the country saw a shortfall after the devastating floods in 2022. Cotton and wheat shortages in the country aggravated the economy’s capacity to produce crops at a larger rate, which it has failed to regulate. Cotton and other perishable exports are the backbones of Pakistan’s exports, with the overall crop situation of the country posing a bigger inflationary risk than others.

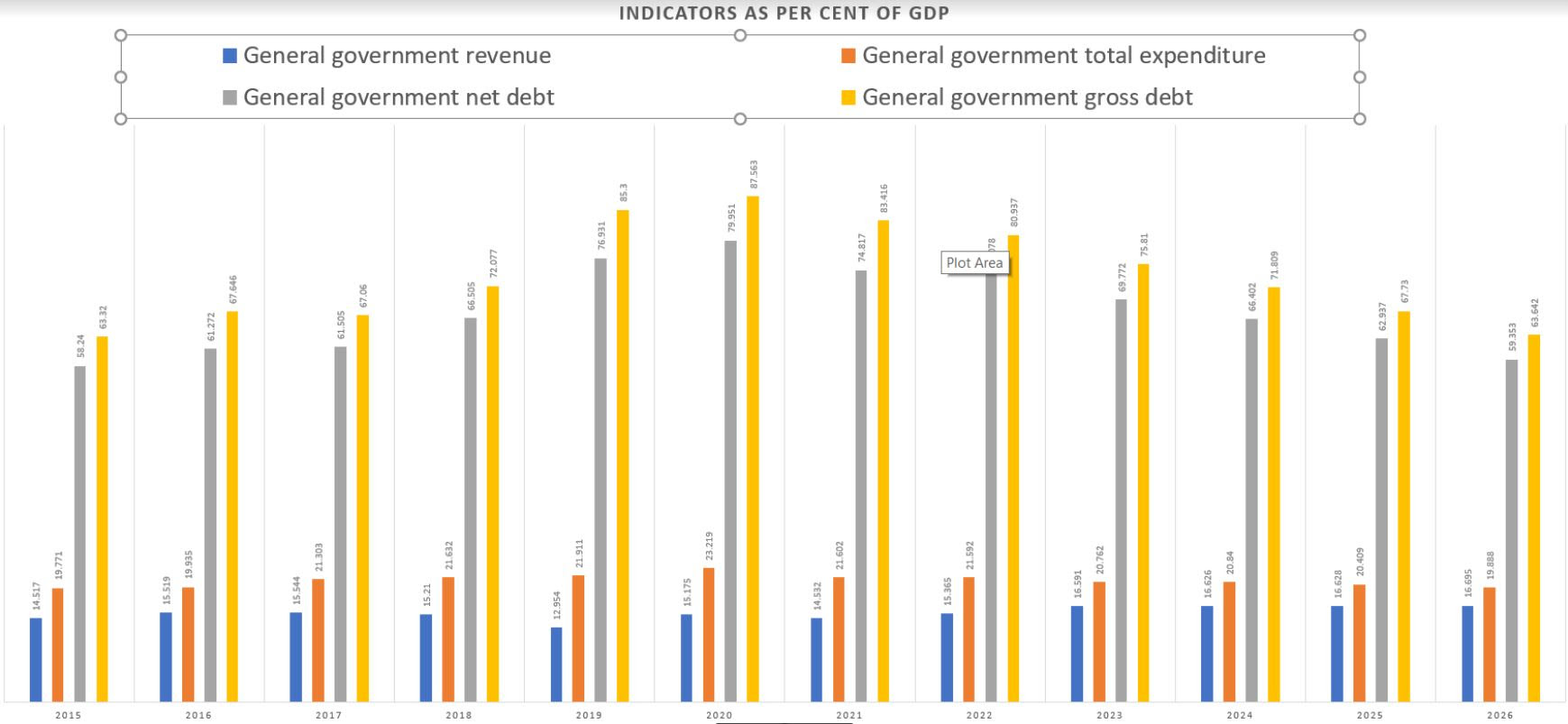

Third, unfavourable rupee value. The policy rate in the country remains largely obsolete, with the economy scouring for larger funding than what is already provided. If the IMF decides to provide a larger concession to the country, the SBP foreign exchange reserves would nearly touch the USD 8-10 billion mark, allowing exporters and traders in the country to import with a larger fiscal space, however, if inflation persists due to structural constraints, the comfort from IMF financing will dissipate.

Fourth, high systemic financial risk. The country is facing an inadequate liquidity crisis, with traders complaining of a “cash squeeze” and Pakistan requiring nearly USD 35 billion for its debt servicing to accommodate global interest rates and allow economic management to comprehend the possible impact of rising debt and servicing issues in the future.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)