Pakistan Reader# 487, 26 December 2022

Ankit Singh

On 24 December, News International reported that IMF had given Pakistan three weeks to implement required actions to enable the release of USD 1 billion to revive the loan program. The virtual talks for the ninth review meeting have been stalled for over a month now. To add further, remarks by the prime minister and other ministers have not boded well with the stock market in Pakistan.

On 22 December, the State Bank of Pakistan, in its weekly report, mentioned that the forex reserve with it had reduced to USD 6.1 billion, an eight-year low. Other banks have a forex reserve of up to USD 5.8 billion. There is speculation that Pakistan might default on its loans while politicians still feel that the country is too big to fail. Previous IMF programs had benchmarks and conditionalities to consolidate the government’s fiscal situation and initiate structural reforms.

Three reasons could be identified for the IMF-Pakistan differences the IMF and Pakistan to opposing ends, yet again.

1. The circular debt in the power sector

Mehtab Haider in his column (The News International) reported that the net losses which the energy sector (gas plus power) currently absorbs are around USD 20 billion. IMF has asked Pakistan to increase tariff. The circular debt in the power sector is about USD 8.75 billion, out of which a subsidy of USD 5 billion is provided by the State and the rest of USD 3.75 billion are to be sourced through fuel adjustment program and loans.

The IMF has also asked Pakistan to reduce the burden of PKR 65 billion (USD 325 million) through fuel price adjustment of last summer, when the demands peaked. While IMF has demanded that revision of the Circular Debt Management Plan (CDMP), that the government considers any additional hike in tariff will come with an exceptional political cost. When compared with countries that have the same per capita income, (for example, Cambodia, Senegal and Kyrgyzstan) Pakistan has the lowest price of one unit of power. When compared with countries with similar population figures, power tariff in Pakistan is cheaper (USD 0.054 per unit); Brazil (USD 0.197 per unit), Mexico (USD 0.088 per unit) and Indonesia (USD 0.093 per unit) are charging more. In South Asia, electricity in Pakistan is cheaper than in Bangladesh and India. So, on a global scale, IMF could still see scope for generating more revenue and consolidation in the Pakistan’s power sector.

2. Market-led exchange rate

Currently, there are three values of PKR against the dollar in Pakistan, open market rate, interbank rate and black-market rate.

Values in the open market rate (PKR 232.5 per USD), interbank rate (PKR 222 per USD) and grey-market rate (PKR 250 per USD) indicate that there is a wide range in the value of the currency and a lot of speculation around the trends. On this, IMF has demanded that the PKR should be allowed to achieve its true exchange rate so that the range is minimised and remittances which are coming through informal routes due to higher commission comes back through formal channels.

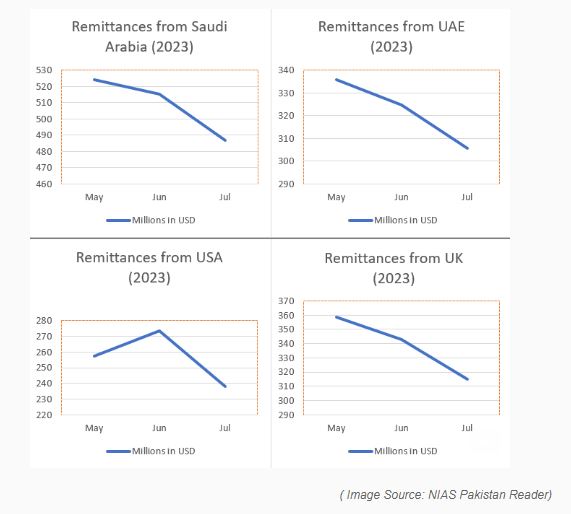

Remittances have dropped by almost 10 per cent during Jul-Nov FY23 and banker and currency experts have attributed the drop to the wide gap in dollar rates. The IMF Mission Chief to Pakistan has also shared his apprehensions with the finance minister that the value of PKR against USD was artificially controlled. Seeing the tough economic conditions and the government’s inability to finance its fiscal deficit, the cornered authorities have prioritized tackling inflation. The present government cannot afford a market-based value of PKR, which can further weaken PKR against USD.

3. Revenue benchmarks and constrained public spending

After becoming the PM, Shehbaz Sharif brought an ordinance prohibiting expensive imports until further notice, to stop the outflow of dollars from cash-strapped Pakistan. This reduced the current account deficit; however, revenue also decreased as a major contributor to the net revenue in Pakistan is non-tax revenue. Collection through customs duties on expensive imports of Pakistan was consequently curtailed.

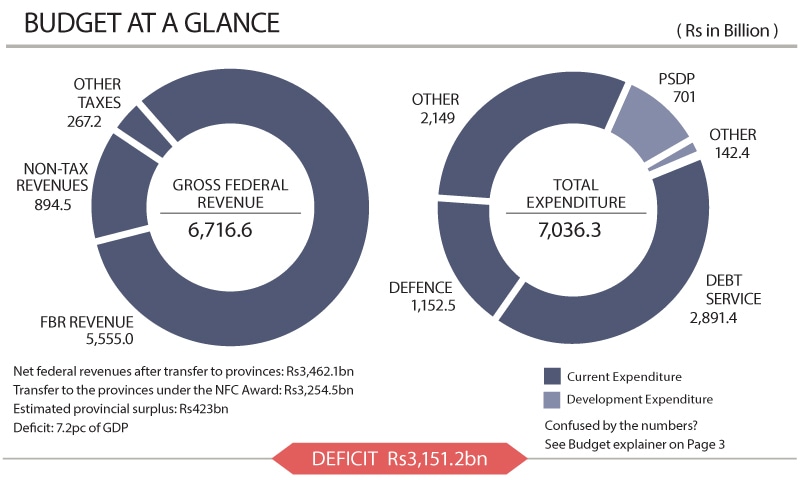

The FBR in its meeting with the IMF last week, had discussed no further need for increasing taxes to reach the targeted revenue of PKR 7.47 trillion (USD 33 billion) and pleaded that FBR would achieve the revenue targets. However, according to IMF’s reporting mechanism, there will be a shortage of PKR 422 billion (USD 2.11 billion). The government has also carried forward shielding consumers from heightened petrol prices and provided subsidies; in October, the government announced providing subsidized petrol to export-oriented sectors, which can further hurt the fiscal position of the government. So, the only sector through which revenue can be juiced out is the public sector enterprises (PSE), IMF has demanded the privatisation of PSEs for the last three decades and reforms on that tangent are yet to fructify.

To conclude, Pakistan is constrained in terms of options to convince IMF of their commitment to utilise its funds in fiscal consolidation. The reality of two streams of Pakistan has never been more evident - affluent Pakistan is making sure the rents and profit flow with subsidies and circular debt; while the lesser Pakistan is going through an inflationary cycle. And the IMF wants to improve fiscal and monetary governance.

The present government also is reluctant from taking hard decisions; the only difference now is that guarantees from friendly countries are conveyed to IMF before the conclusion of review meetings. The media has been circulating news on the same. The IMF, instead of tapping to external financing, is turning other way round, from external financing guarantees to an approval tap and discussions will go as usual.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)